How to Raise Money for Your Quantum Company Part II

Part II: Typical Investment Terms

In Part I of this post, I described the overall funding landscape and provided some suggestions on how to navigate through it (you can read that post here). In Part II I’ll cover some typical venture deal terms and structures. This comes with the usual caveat in that there are no hard-and-fast rules about these things and different investors have different processes and expectations so consider the subjects in this post as broad guidelines. I sometimes refer to the investors as “Venture Capital” firms or “VCs” but much of this applies to any investor.

Valuation: Pre-Money vs Post-Money

There is a lot of financing jargon that is not intuitive and so can appear intimidating. Hopefully this post will give you more comfort when having conversations with prospective investors. One of the most essential focus points of such discussions will be about “valuation.” This is important for a number of reasons, most notably because it will drive the dilution existing investors would face. Very simply, the higher the valuation, the lower the dilution.

The confusion with “valuation” is usually around the difference between “Pre-Money” value and “Post-Money” value (venture investors may shorten this to saying “Pre” and “Post”, dropping the “Money” part). But don’t let this trip you up…it’s quite simple algebra:

Post-Money Valuation = Pre-Money Valuation + Amount Invested

If you parse this down and think about it logically, let’s say your company today is worth $10 million. That $10 million is the value today, before new money is added. If you raise $5 million which is then contributed to the company’s balance sheet, the company should be worth its original amount ($10 million) plus the new money contributed or a Post-Money valuation of $15 million.

The investor’s share of the business is always calculated off of Post-Money value, so in this case they would have $5 million of the $15 million in Post-Money value or 33.3%. There is often confusion because VCs generally discuss Pre-Money valuation, but their share is calculated Post-Money. It seems confusing but if you can sort out quantum mechanics you can sort this out!

Process

As you would expect, there is a courting ritual that most investors and companies will go through. In the early interactions both parties are getting to know each other broadly and will attempt to assess whether or not they want to invest energies into trying to reach a deal and commit the necessary resources. Below is a very crude process map:

And here is a brief summary of each step:

Early Diligence: This process can be quick or can take quite a long time, and it really is a two-way process meaning the investor will be trying to assess their interest, but the target company should also do its own diligence to see if they feel that the investor would be a good fit and whether it brings value beyond just the money. Generally, assuming both parties agree to get more serious, a Confidentiality Agreement is typically entered into at some point of this stage, although typically not at the beginning (see Part I for more on this).

Letter of Intent (LOI): While this step is sometimes skipped, it’s a good first gate point. Typically, it is crafted by the prospective investor, is non-binding and lays out their general thoughts about an investment including value or valuation range, form of investment, estimated timeline and next steps, among other details.

Term Sheet/Heads of Terms: A bit more formal than a Letter of Intent, this gets much more granular about the specific terms of an investment. Nearly always, the investor will demand some period of exclusivity (generally as short at 2 weeks or as long as 2 months) because they will dedicate meaningful resources which might include paying lawyers or professionals to participate in the diligence and so will want to know that if they follow-through with the stated terms, they won’t have some other buyer swoop in and steal the deal. This document is also generally non-binding, other than the exclusivity and confidentiality terms.

Deeper Diligence: While you may be frustrated with all the diligence already done, here is where it gets quite serious. And while it may feel like there are already signatures on paper with the Term Sheet so you must be close, many deals fall apart at this stage. If you have been untruthful or have withheld things during preliminary diligence, here is where that will come to bite and would likely derail any deal because of credibility issues. So being forthcoming and honest from the beginning is the best strategy in the long term. And to be forewarned, diligence can be excruciating and time consuming. Most investment firms like VCs take money from limited partners so have a fiduciary duty to those partners to turn over every stone and make sure there are no surprises that come out post-acquisition. A tricky part of this process involves customer contacts. Often a buyer will want to speak with your top customers directly, and you may not want to spook any of them until/unless absolutely necessary so it’s reasonable to have this be one of the very last steps before finalizing the deal.

Purchase Agreement: This comes in various forms and names but refers to the definitive deal document which will be signed prior to receiving the investment. If the Term Sheet was extensive and well thought out, the Purchase Agreement should be fairly routine to complete, although it will be more extensive and often times there are specific terms or details that can still upset the process. It can be laborious and intimidating, especially if you have not been involved in one before but be patient and supply all the needed pieces. A common stumbling provision can be the” Representations and Warranties” section which is where the Company/Owners will affirm all manner of balance sheet items in excruciating detail. For example, one provision in this section may be “contingent liabilities” and may you think that it best to leave that blank for anything that may be threatening but not yet real. For example, let’s a say a customer was unhappy with a large order they received from you. If you leave the contingent liability section silent on that, and that client then demands to return the product and/or get a post-closing refund, the original owners would be responsible (there will be some purchase price set aside in escrow for a period to cover things like this). However, if you listed “we have one disgruntled customer and although no claims for returns have yet been made, this is something we are watching carefully,” as a contingent liability and the buyer still completes its investment, if that client ultimately comes forward for a refund, it will be a company obligation and will not come out of escrow.

Closing: Generally, the prior steps can take 3-6 months (or sometimes longer) from start to close and both parties are typically equally excited to finally complete the deal. Usually “signing” of the purchase agreement and funding happen on the same day, but sometimes there is a lag of a few days or weeks, especially if certain consents or other third-party agreements are required, or if there is a compelling reason to have the closing on a specific fiscal date.

Debt vs. Equity

There are two broad ways that investors will participate in a business: Equity and/or Debt.

Equity: This is a typical form of venture investment and involves having an investor make an investment for a number of shares or units in the company and is therefore dilutive to original/existing owners. Within this bucket are a few different flavors:

Common Stock: This is the most typical form of equity and usually includes one vote per share. It is the lowest priority in liquidation events but is usually the largest equity item on the balance sheet.

Preferred Stock: This is usually the form of equity issued to investors and has priority over common stock in a liquidation. It may or may not include voting rights.

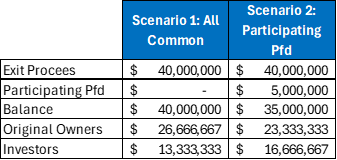

Participating Preferred Stock: This is preferred stock which provides that upon exit it is first repaid, and then the remaining proceeds are split pro rata among all equity investors. The following highlights the difference, assuming a company with a $10m pre-money value, a $5m participating preferred investment, and then a sale for $40 million:

You’ll note that the investors received and “extra turn” on their investment and so while they own 33.3% of the company, they actually receive 42% of the proceeds. This is a 1x participating preferred. Some investors will seek 2x which enhances their return even further.

Debt: Some businesses can borrow money to finance their business, or may sell “convertible notes” to investors, which typically feature some aspects of “debt” and some of “equity.” A very common construct for early investors is to invest via “SAFE” notes which stands for “Simple Agreement for Future Equity.” SAFE notes generally have a few key provisions:

Modest Amounts: Often these are sold to friends and family or others that are close to the company, commonly in $50k-$250k amounts per investor.

Interest Rate: These notes generally include a single-digit interest rate (i.e., 6%-8%) which accrues but is not paid (known as PIK interest or payment-in-kind).

Conversion Price: Typically, these notes automatically convert to equity in the future, as part of a subsequent equity raise, and the conversion is usually at a 10%-20% discount to that future raise. This avoids the need to negotiate equity valuation at the time these notes are sold. However, as a caveat, if a qualifying equity round is not completed by the time the notes mature (typically 18-26 months), the monies need to be repaid.

Conversion Cap: Sometimes there is a top to the valuation of the conversion and often this is combined with the Conversion Price, in which case the conversion will be at the lower of the conversion price or some agreed upon maximum value.

Rolling Close: Often these can be sold over some rolling period of time with the company able to use the proceeds as it collects the funds.

Liquidation Preference: These notes are usually more senior than any of the equity (i.e., would be repaid before equity in a liquidation) and often times have a multiplier included (typically 1x-3x). If there is a 2x liquidation preference and the company is acquired before any qualifying equity round is completed, the SAFE notes investors would receive the higher of 2x their original investment, plus accrued interest or the amount valued upon conversion.

There are many other forms of debt, which is nearly always less costly to the business than equity, although harder to get, particularly for early start-ups without substantial assets.

On a personal side note, there is also something called Venture Debt which can be available if the company has substantial IP or other intrinsic value. The Venture Debt lender fully securitizes their loan against the asset and are repaid out of revenues, typically at somewhat elevated interest rates, with equity kickers and with aggressive rights to control operations if you miss your forecast. The underwriting can be quite expensive and would need to be paid for by the borrower. I can’t endorse these types of structures.

Additional Transaction Terms

It’s difficult to succinctly summarize typical transaction terms because all deals and investors are different, but here are a few terms you can likely expect will be required by investors.

Anti-Dilution: Investors may demand protection from future dilution, especially from down rounds. A “full ratchet” essentially re-prices the original investment at the new lower price and is quite aggressive and not often granted. More typically, the investor will demand and receive a right to invest in new rounds for whatever amount enables their percentage ownership to remain unchanged (sometimes also referred to as Pro-Rata rights).

Drag-Along Rights: Enables a majority of investors to force minority owners to join in a sale. This is important because prospective future acquirors may only be interested if they can acquire 100% so if a small investor refuses to sell, and there are no drag-along rights, they could kill the deal.

Tag-Along Rights: Enables an investor to share, pro rata, in any future sale. For example, if Investor A wants to sell their position and Investor B has these rights, they can force the buyer of Investor A shares to also buy their shares (or some pro rata split between A and B).

Right of First Refusal (ROFR): Gives the investor the rights to purchase new shares before they can be sold to outside parties. This seems innocuous but is onerous on the company because it typically scares off offers from third parties.

Right of First Offer (ROFO): Gives the investor the right to make the first offer if the company decides to sell or raise more equity. Much less onerous on the company than a ROFR.

Option Pool: The investor will typically require setting aside a 10%-20% pool of options for employees. Often, they will demand that this pool only dilutes the original owners, not their investment.

Board Seats: Many investors will demand some board representation so they have a seat at the table for any significant events, and some will require the addition of some outside directors. While this is often fair, entrepreneurs should be very careful and should anticipate that if future rounds are raised with new investors, they too may require board seats. In many instances, statutory seats are not provided but instead “board observer” rights are granted, meaning the investor is privy to all board materials and can have a representative attend meetings, although they cannot formally cast board votes.

Governance: Early venture investors who do not buy more than 50% of the business, will not have the ability to control the business, so will expect certain contractual protections. Typically, this includes things like requiring the prior approval before raising more equity, changing the compensation of the executives, changing the nature of the business and certain other significant changes.

Key Man Insurance: If there are crucial founders or executives, the investors may require that the company purchase life insurance policies on those individuals, with the company as beneficiary. The logic is that this would provide resources to the company to replace key employees.

Naturally there are other terms and provisions and there are no hard and fast rules for what terms may be included or what the specific details may be.

Other Suggestions

Get Strong Counsel: Hiring the right law firm will be vital for companies seeking venture investment, and you should be prepared for it to be quite pricey. I strongly suggest you do not try to use your relative or some discount-priced sole practitioner because this is a crucial transaction and will have wide and long-lasting effects. Find a law firm with substantial transactional experience which will be expensive in the short run but will help ensure long-term success.

Prepare for Diligence in Advance: I can’t state this more plainly…diligence will be excruciating. You will be asked to provide all manners of documentation and financial schedules including tax returns. Having this ready in advance will substantially help the process. Your lawyer will be able to help you with this.

Mind your Structure: You may want to consider “cleaning up” your structure and possibly converting to a C-Corp. The more buttoned-down you are in advance, the less likely a buyer will be spooked or put off by your structure. If you have “promised” equity or phantom equity or other things to employees, be sure that is all properly documented and cleaned up in advance.

Have Credible Financials: Your historical financial results should be up-to-date and clean, with all inflows and outflows properly recorded and reconciled. If possible, have audited financials prepared and if not have reviewed financials at a minimum. While investors will be compelled to make the investment based on your technology or strategy, they will also expect the books and records to be orderly.

I usually try to have Quantum Leap posts demystify quantum, especially from an investor perspective, but I hope this two-part series helps demystify the investment process for quantum entrepreneurs. I want to reiterate that much of this is a high-level summary of some typical processes and terms, but every deal is unique, and any investment is a give-and-take negotiation.

Disclosure: I wrote this article myself and express it as my own opinion. The content provided is for informational purposes only and should not be construed as financial or investment advice. Readers are advised to consult with a qualified professional before making any investment decisions. The author of this blog shall not be held liable for any losses, damages, or consequences resulting from the use of this information.

Further Reading: Here are a few resources that may help you further understand these market dynamics:

https://carta.com/learn/equity/common-stock-vs-preferred-stock/

https://en.wikipedia.org/wiki/Participating_preferred_stock

https://www.embroker.com/blog/startup-venture-capital-terms/

https://www.goingvc.com/post/the-ultimate-guide-to-venture-capital-term-sheets

https://www.svb.com/startup-insights/vc-relations/venture-capital-term-sheets/

https://venturecapitalcareers.com/blog/vc-glossary

Citations:

In addition to the resources noted above, further content provided by:

Perplexity. (2025) Perplexity.ai (AI Chatbot) [Large Language Model].

Great resource!